The Rise of Super Apps: Why They Matter in Our Digital Ecosystem

In today’s increasingly digital world, the concept of “Super Apps” has emerged as a powerful paradigm shift in how we interact with services and manage our digital lives. Recently, Sri Lanka made headlines with the introduction of GovPay - not as a standalone application, but as a service integrated into existing platforms like Helakuru and Frimi. This strategic decision highlights a growing global understanding of super app ecosystems and their benefits.

What Exactly Is a Super App?

A super app is a single mobile application that offers a wide range of services and functionalities that would traditionally require multiple separate apps. Think of it as a digital Swiss Army knife - one tool with many functions rather than carrying a separate tool for each task.

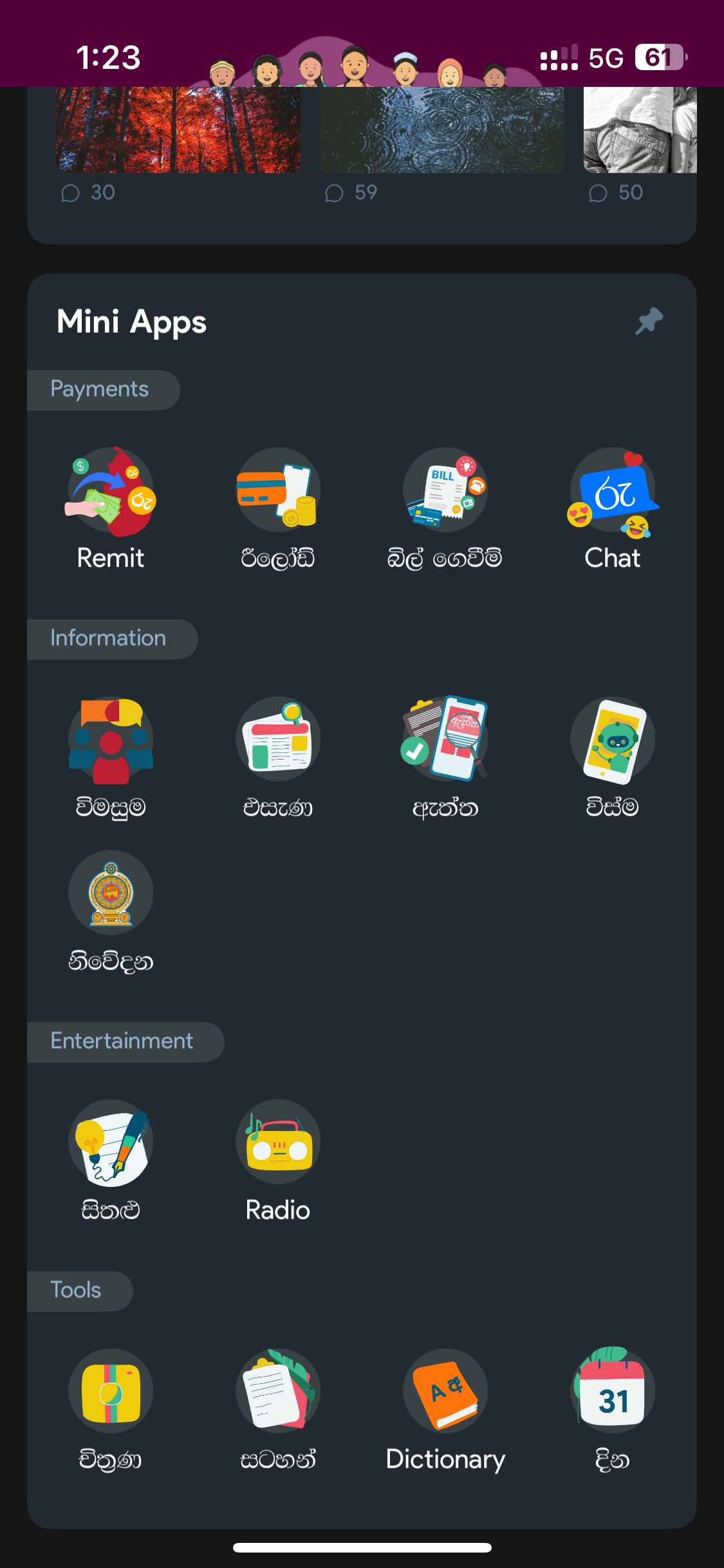

Helakuru : Sri Lanka's leading super app with multiple services

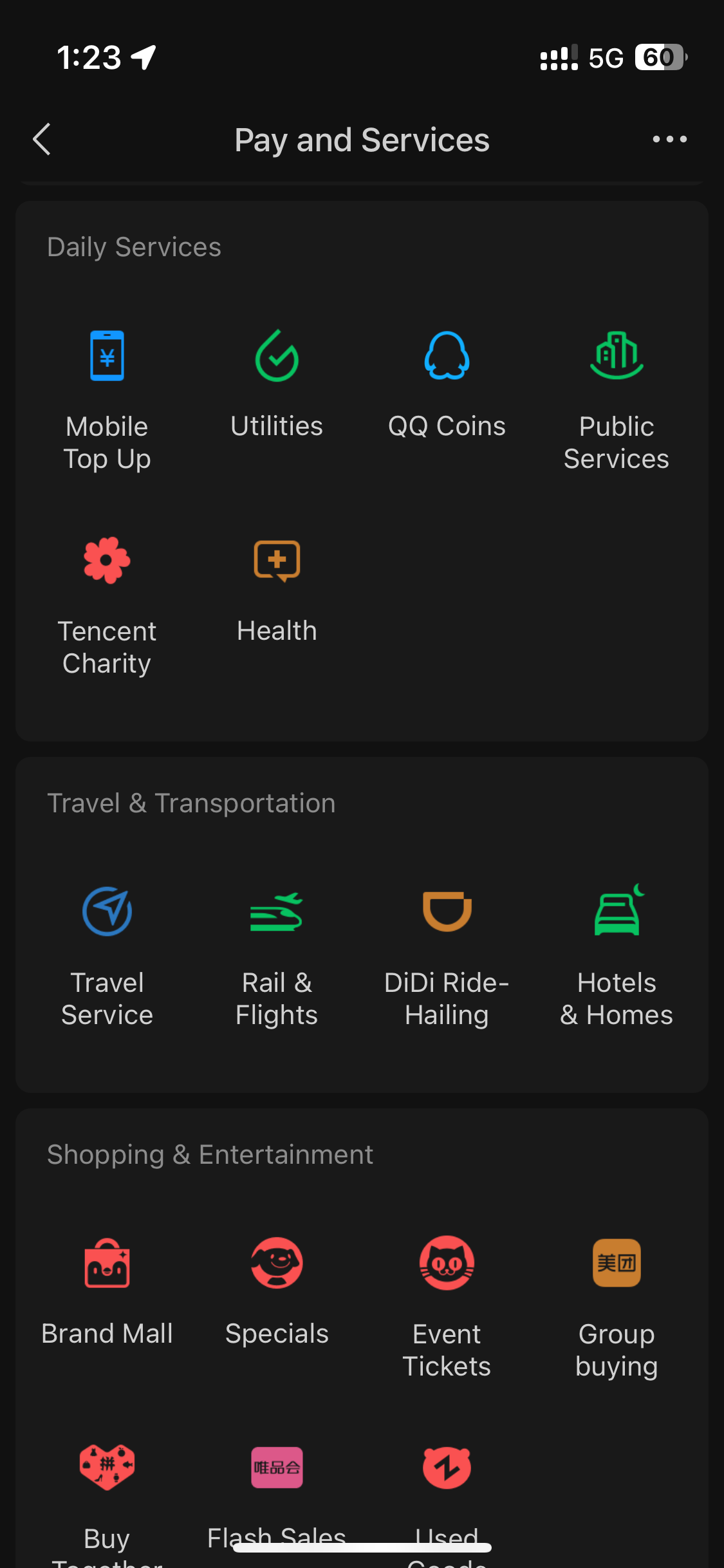

WeChat: China's pioneering super app ecosystem

The Super App Formula: Solving Real Problems First

For a super app to emerge and succeed in any market, it must follow a specific formula that begins with addressing a fundamental need.

Step 1: Fix a Burning Issue

The foundation of any successful super app is its ability to solve a real and pressing problem. WeChat in China began by addressing the need for efficient messaging. Helakuru in Sri Lanka gained traction by solving the challenge of typing in Sinhala. This initial “hook” creates the necessary user base that can later be leveraged for expanded services.

Step 2: Build a Strong Identity Framework

Once users are on board, super apps need a robust identity service. This includes gathering and verifying basic information such as names, addresses, phone numbers, and email addresses. This identity layer becomes the foundation for all other services within the ecosystem.

Step 3: Implement a Payment Processing Engine

The payment infrastructure is perhaps the most critical element in transforming a popular app into a super app. This can be implemented in two main ways:

- Real-time processing: Fetching funds directly from a bank account or card at the time of transaction

- Wallet-based system: Allowing users to store value within the app itself through top-ups from bank accounts, cards, or peer transfers (similar to WeChat Pay and AliPay)

These payment systems can connect through:

- Internet payment gateways (IPGs) linking to card networks like Visa, Mastercard, Amex, or UnionPay

- Country-specific aggregators like LankaPay (Sri Lanka) or UPI (India)

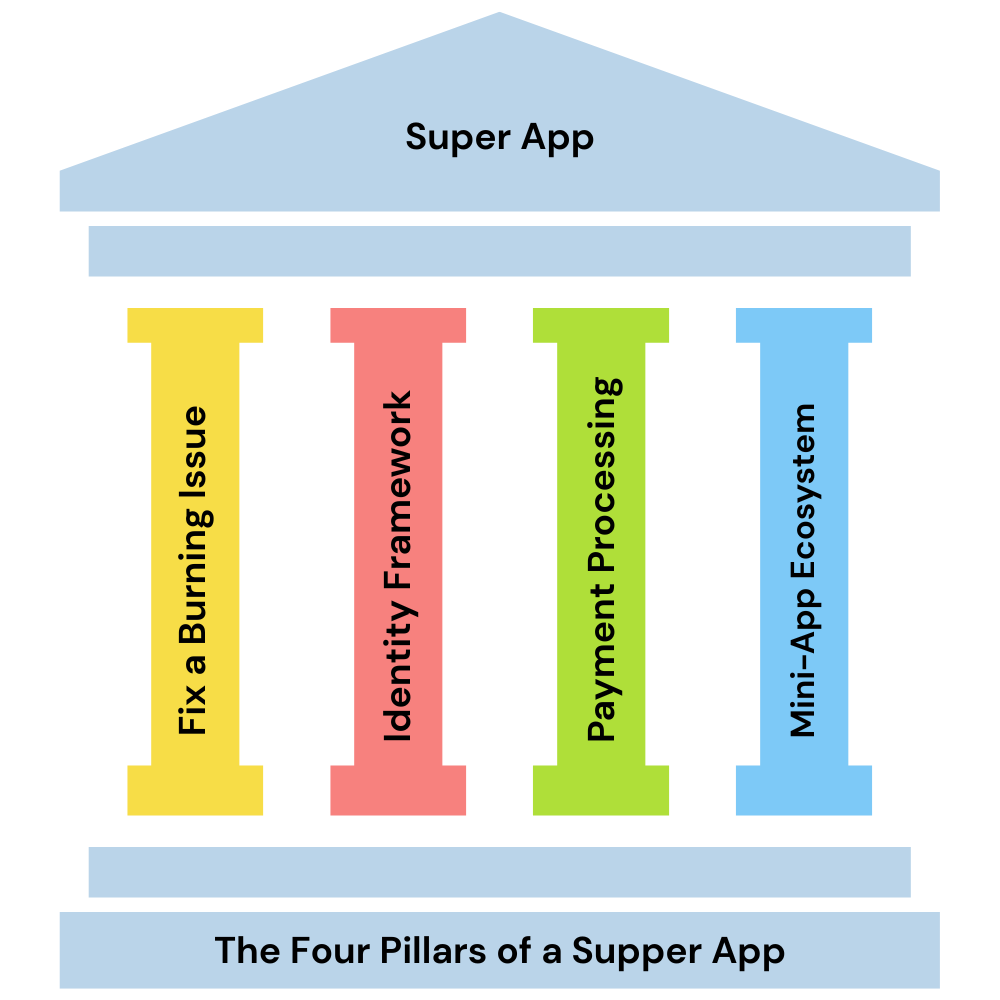

Step 4: Create an Open Mini-App Ecosystem

The final piece of the puzzle is developing an open platform that allows third-party services to build within the super app’s ecosystem. These mini-apps leverage the core identity and payment services already established by the host app.

The host app typically has extensive permissions on the user’s device, including access to WiFi, Bluetooth, camera, GPS, gyroscope, fingerprint, and facial recognition. This creates a responsibility dynamic where users trust the host app, which in turn governs and evaluates the mini-apps published on its platform.

The four essential pillars for building a successful super app

The Super App Advantage

The primary benefit for users is simplicity. With a super app, there’s no need to create new accounts or add payment details across dozens of different services. One login, one payment setup, multiple services - creating a frictionless digital experience.

Comparing Digital Ecosystems: East vs. West vs. Sri Lanka

| Service | Western Countries (US, UK, etc.) | Sri Lanka | China |

|---|---|---|---|

| Chatting | WhatsApp, Messenger, iMessage | WhatsApp, Viber, Messenger | WeChat (core function) |

| Food Ordering | Uber Eats, DoorDash, Deliveroo | PickMe Food, UberEats | Meituan (standalone + WeChat mini-app), Ele.me (standalone + Alipay mini-app) |

| Taxi/Ride-hailing | Uber, Lyft, Bolt | PickMe, Uber | DiDi (standalone + available as mini-app in WeChat & Alipay) |

| Ticket Purchasing | Ticketmaster, Trainline, Airline apps | Bus.lk, Train booking sites, individual cinema apps | Multiple services as mini-apps within WeChat & Alipay ecosystems |

| Loyalty Programs | Individual store apps, Stocard | Individual store apps | Integrated directly into WeChat & Alipay mini-apps for most major retailers |

| Payments/Money Transfer | Venmo, Cash App, PayPal, Banking apps | FriMi, LANKAQR apps, Banking apps | WeChat Pay, Alipay (core functions of their respective super apps) |

| Shopping | Amazon, eBay, Walmart | Daraz, Kapruka | Taobao, JD.com, Pinduoduo (all available as standalone apps and as mini-apps in WeChat & Alipay) |

| Government Services | Multiple government websites/apps | GovPay (via FinTech apps), Gov.lk | Multiple government services integrated as mini-apps in WeChat & Alipay |

| Health Services | MyChart, Zocdoc, Individual provider apps | eChannelling, Doc990 | Hospital appointment booking, health records, insurance claims all as mini-apps in WeChat & Alipay |

| Education | Canvas, Blackboard, Khan Academy | Various standalone apps | Online courses, tutoring services, and educational resources as mini-apps in WeChat & Alipay |

As you can see from the comparison, the Western digital landscape remains largely fragmented, with users juggling dozens of apps for different services. China, on the other hand, has consolidated most digital interactions into two major super apps: WeChat and Alipay. Sri Lanka appears to be on a path between these models, with some consolidation beginning around platforms like Helakuru and financial service apps.

Understanding Sri Lanka’s Digital Payment Infrastructure

LankaPay: The Financial Backbone

LankaPay is Sri Lanka’s national payment infrastructure that functions as the backbone connecting financial institutions across the country. Think of it like the “highway system” for financial transactions:

- It’s the underlying technology that allows banks and financial institutions to communicate

- It processes interbank transactions securely and efficiently

- It’s not a consumer-facing app but rather the invisible infrastructure

- It enables functions like real-time fund transfers between different banks

In simple terms, when you transfer money between banks in Sri Lanka, LankaPay is what makes this possible behind the scenes.

LANKAQR: The Universal Payment Code

LANKAQR deserves special recognition as a forward-thinking approach to digital payments. LANKAQR is a standardized QR code system that runs on the LankaPay infrastructure - think of LankaPay as the engine under the hood, while LANKAQR is the steering wheel that lets users control it.

Let me explain with a simple example:

Imagine LankaPay as the country’s water supply system - the pipes, pumps, and purification plants that connect every home. Most people never see this infrastructure, but they depend on it daily.

Now, LANKAQR is like having a universal tap design that works in every home, hotel, and business. No matter whose building you’re in, you know exactly how to turn on the water because all the taps work the same way.

In practical terms:

- When a small restaurant displays a LANKAQR code, customers can scan it with any compatible payment app (FriMi, HNB SOLO, SDB Wallet, etc.)

- The transaction request travels through the LankaPay infrastructure to complete the payment

- Merchants don’t need separate QR codes for different payment apps

- Customers can use whichever app they prefer

A Different Approach from China’a WeChat and AliPay

China’s super app ecosystem with WeChat Pay and Alipay has been remarkably successful at creating seamless digital experiences. Their model is built around:

- Large ecosystems with mini-apps integrated into the payment platforms

- Primarily wallet-based systems where users store value within the app

- Deep integration with the respective super app environments

Sri Lanka’s approach with LANKAQR offers a different but equally innovative path by emphasizing interoperability and open standards. Rather than having separate QR systems for each payment provider, LANKAQR creates a unified standard that works across different apps while still allowing each to compete on features and user experience.

Both approaches effectively serve their markets. China’s model has driven massive adoption and created incredibly convenient consumer experiences. Sri Lanka’s model promotes competition while maintaining convenience for both merchants and consumers.

GovPay: Building on Existing Infrastructure

By integrating GovPay with existing apps through LankaPay infrastructure and the LANKAQR standard, the Sri Lankan government has made a smart choice to meet citizens where they already are digitally. This reduces friction in adoption and demonstrates an understanding that the most successful digital services often build on existing user behavior rather than trying to change it.

This pragmatic approach could serve as a model for other governments looking to expand digital service delivery without creating an ever-growing collection of standalone apps that citizens must download, register for, and learn to use.

Conclusion

The government’s decision to integrate GovPay with existing apps rather than launching yet another standalone service demonstrates a sophisticated understanding of digital ecosystems. By leveraging platforms that citizens already use and trust, the adoption barrier is significantly lowered.

As more countries navigate the balance between convenience and openness in their digital infrastructure, the lessons from super apps will continue to shape how we interact with services in our increasingly connected world. Whether Sri Lanka will ultimately follow China’s path toward super app consolidation or forge its own hybrid model remains to be seen, but the foundations for both possibilities are now clearly being laid.

For citizens, businesses, and governments alike, understanding the super app paradigm isn’t just about technological trends, it’s about recognizing a fundamental shift in how digital services are delivered and consumed in the modern economy.

Tags

About the Author

Pasan Thilakasiri, PhD

Co-founder & Managing Director

Dr. Pasan Thilakasiri is a digital transformation expert with a PhD in e-governance from Huazhong University of Science and Technology (HUST). He has extensive experience in IT consulting, system integration, and digital transformation initiatives, including work with the Information and Communication Technology Agency (ICTA) of Sri Lanka on healthcare digitalization projects that have impacted over 9.5 million individuals across 81 hospitals nationwide.

A monthly note for SME operators

On technology, AI, and digitalisation. One real story, two trends, and one quick win each issue.

Recent Posts

Categories

You May Also Like

How We Actually Use AI on Real Customer Work

Eight months of unresolved accounting drift. 3,600 historical transactions. One working session to untangle it, because AI was sitting alongside...

Read More

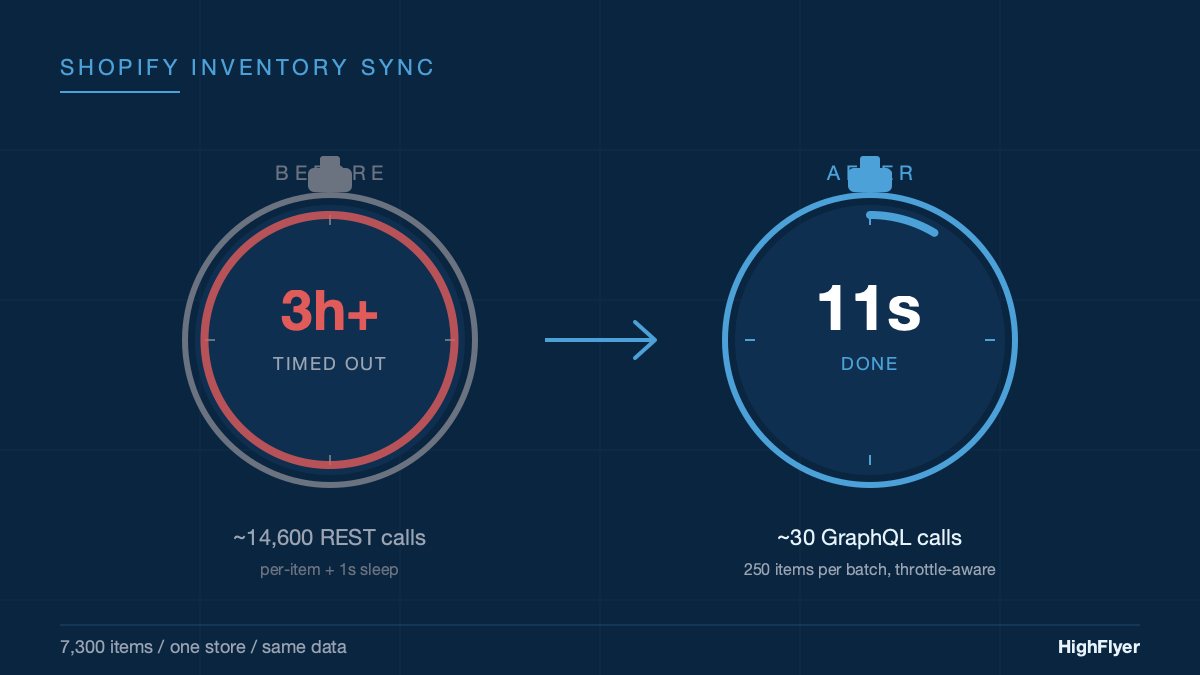

From 3 Hours to 11 Seconds: Fixing a Shopify Stock Sync That Kept Timing Out

We kept bumping the timeout. First to 60 minutes. Then to 3 hours. It still timed out. The timeout was...

Read More

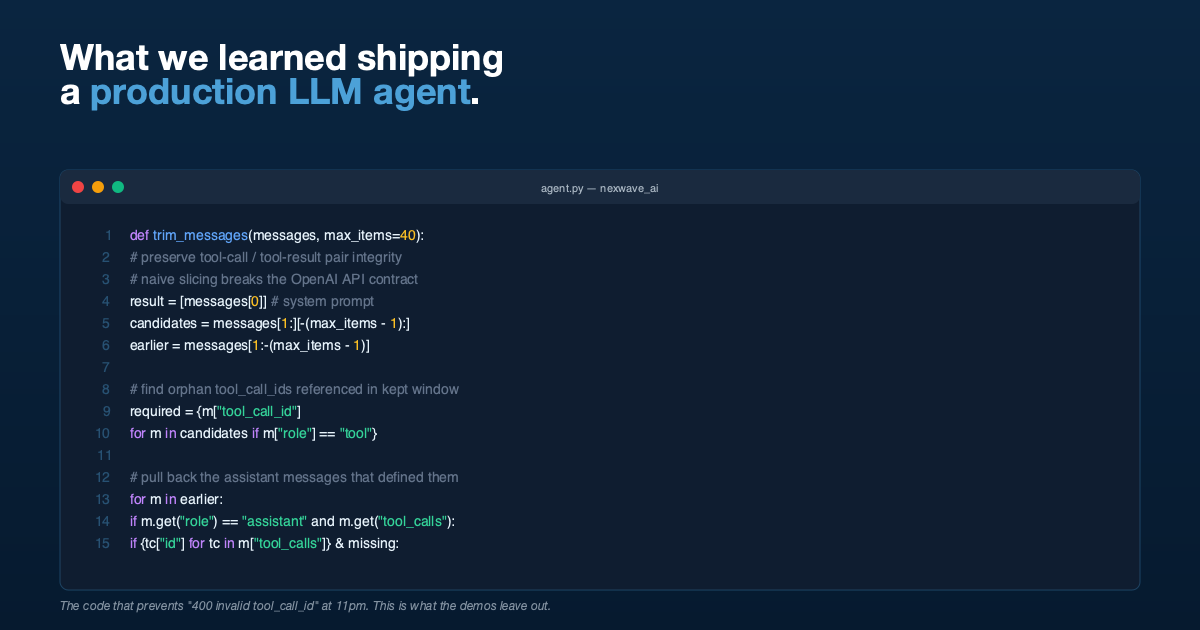

What We Learned Putting an AI Assistant Inside a Live Business System

An AI that gives a finance team an off-by-a-dollar answer loses their trust forever. Here are the five things we...

Read More